Türkiye's economy model: Is it working?

Last Thursday, the Turkish central bank cut the key interest rate unexpectedly by 150 basis points (economists and analysts expected 100 basis points). The benchmark rate is at now at 10.5% from 12%.

But somehow this was still expected. Markets did not show severe reaction: the Turkish lira, stayed around 18,58 against the dollar (after the weekend, however, it lost slightly and is now back at the 18,6 mark). The stock market showed gains (BIST 100 went up by around 1%).

I am not going to discuss the drivers or reasoning behind this decision. International media pretty much covers this topic well (see e.g., the Financial Times).

What I ask myself and what is more intriguing from an economist's point of view is the following: is the so-called “Türkiye economy model” working?

Little background before I answer this question (if you know all this, scroll down to “Is the unconventional economy model working?”):

Why Türkiye economy model?

When inflation in an economy goes up, central banks implement a tighter monetary policy, which in most cases means increasing the key interest rate, at which banks lend money (and companies need for their businesses and investments). Stabilizing prices in such a way has some unwanted consequences: the economy might slow down as borrowing money becomes more expensive.

Back to Türkiye: The country has been suffering from exceptionally high inflation numbers. Prices increase annually, September data shows inflation above 80%. Monetary policy makers would usually tighten the key interest rate of the central bank (or keep it unchanged at a higher level). The broader concept behind this is the following: higher rates (or a tightening monetary policy) reduce money supply due to higher borrowing costs and control domestic currency from inflation. This is a conventional economic theory.

Turkish monetary policy makers, however, do it differently: Last year in September 2021, the Central Bank of the Republic of Turkey (CBRT) started to cut interest rates. Prices kept rising and since December 2021, the currency has been on and off under a fair amount of pressure (since the beginning of 2022 the Turkish lira lost almost 30% against the dollar).

At the end of 2021, Turkish policy makers implemented several measures to stop the fall of the currency and limit inflation. For example, selling dollars for Turkish lira is a common strategy by central banks.

Currency hedged deposit account

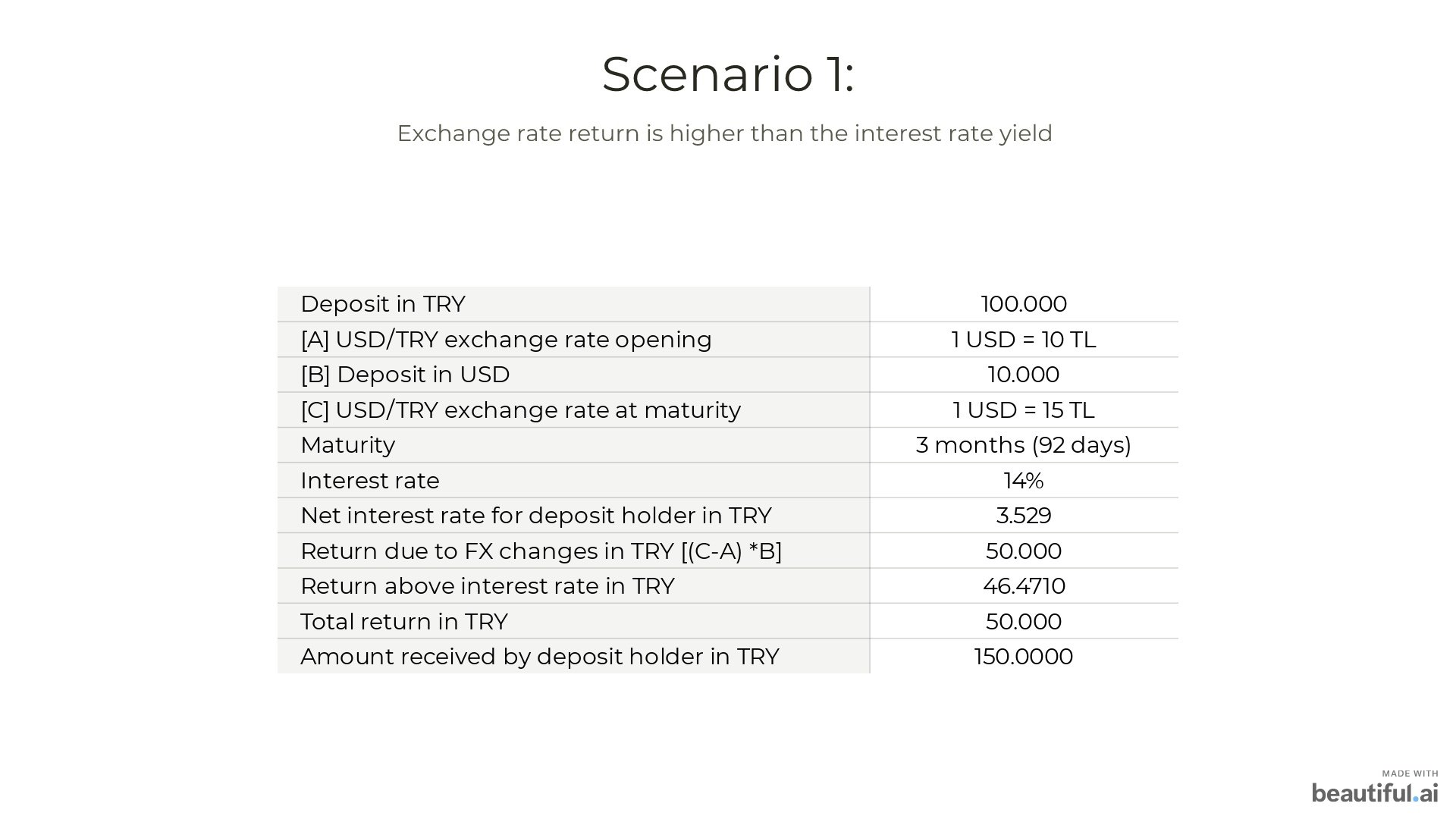

A different instrument, and less common, was the so-called KKM (in Turkish short for “kur korumalı mevduat hesabı” meaning simply in English “currency hedged deposit account”), initially labelled the “Turkish Dollar”. As the name indicates the deposits are secured against currency fluctuations, by paying the difference if the Turkish lira increases by more than the interest rate against the dollar at maturity. In this way, it aims to prevent any foreign exchange rate-related losses of savings and encourages to keep lira deposits in banks.

Let me give you a clear example, what this means for lira deposit holders. First, let's see what happens when the currency keeps depreciating (this is happening in reality).

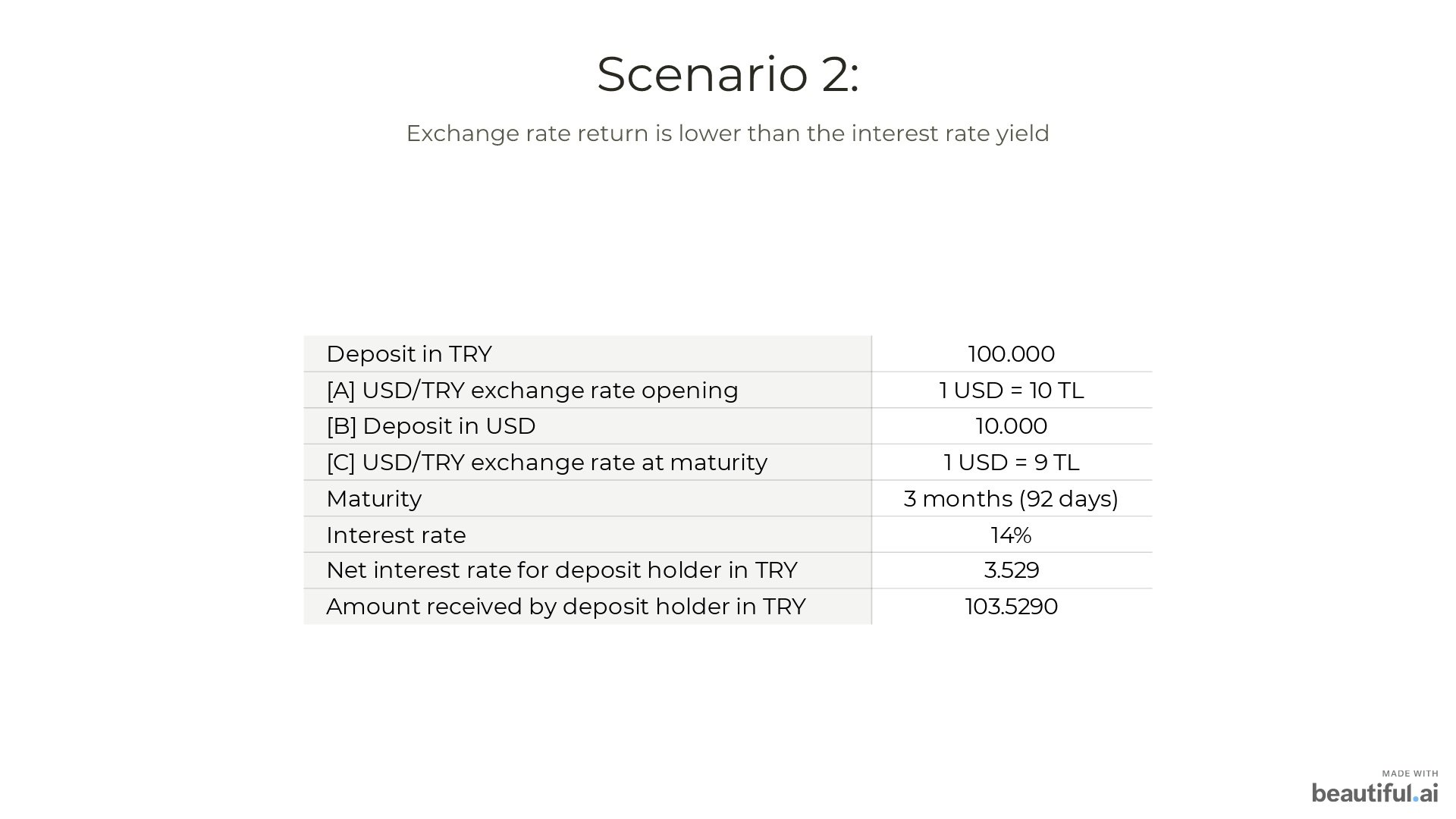

The second example illustrates a case where the lira becomes eventually stronger (which is not happening now).

Is the unconventional economy model working?

At the beginning of 2022, it wasn’t clear what the model entails, how it works, and if it’s successful in stabilizing the lira and ensuring price stability. Now, almost one year later, we have data available and can assess whether the alternative measures are working.

For that, let’s have a look at some economic numbers.

Despite the efforts the lira fell through 18 Turkish lira to the dollar. The Turkish currency lost about half of its value against the dollar today compared to a year earlier and it is still highly volatile. Inflation is high and has not peaked yet. Data from last month show surging prices by 83 % year-on-year. The is the highest level since 1998.

However, this is only one side of the story. Let’s look at the other side, like economic growth, consumption, and production activity. According to Reuters, Goldman Sachs increased the forecast for Türkiye’s 2022 GDP to 5.5% from 3.5%. Türkiye’s spending and credit appetite is propelling growth. Economic activity is solid, there is strong domestic demand, high industrial production and (because of the falling lira) high exports (growth of 16.4% in the second quarter compared to last year).

The aim to keep economic activity growing through the Türkiye economy model seems to work. But this comes at a cost of high inflation, a volatile currency, and additionally increased government spending. Several fiscal stimulus packages have been introduced to mitigate the negative impact of the pandemic and the government has still increased expenditures arising from inflation or currency losses (e.g., increasing pensions and public sector wages). The compensation for the lira losses also comes at a high price.

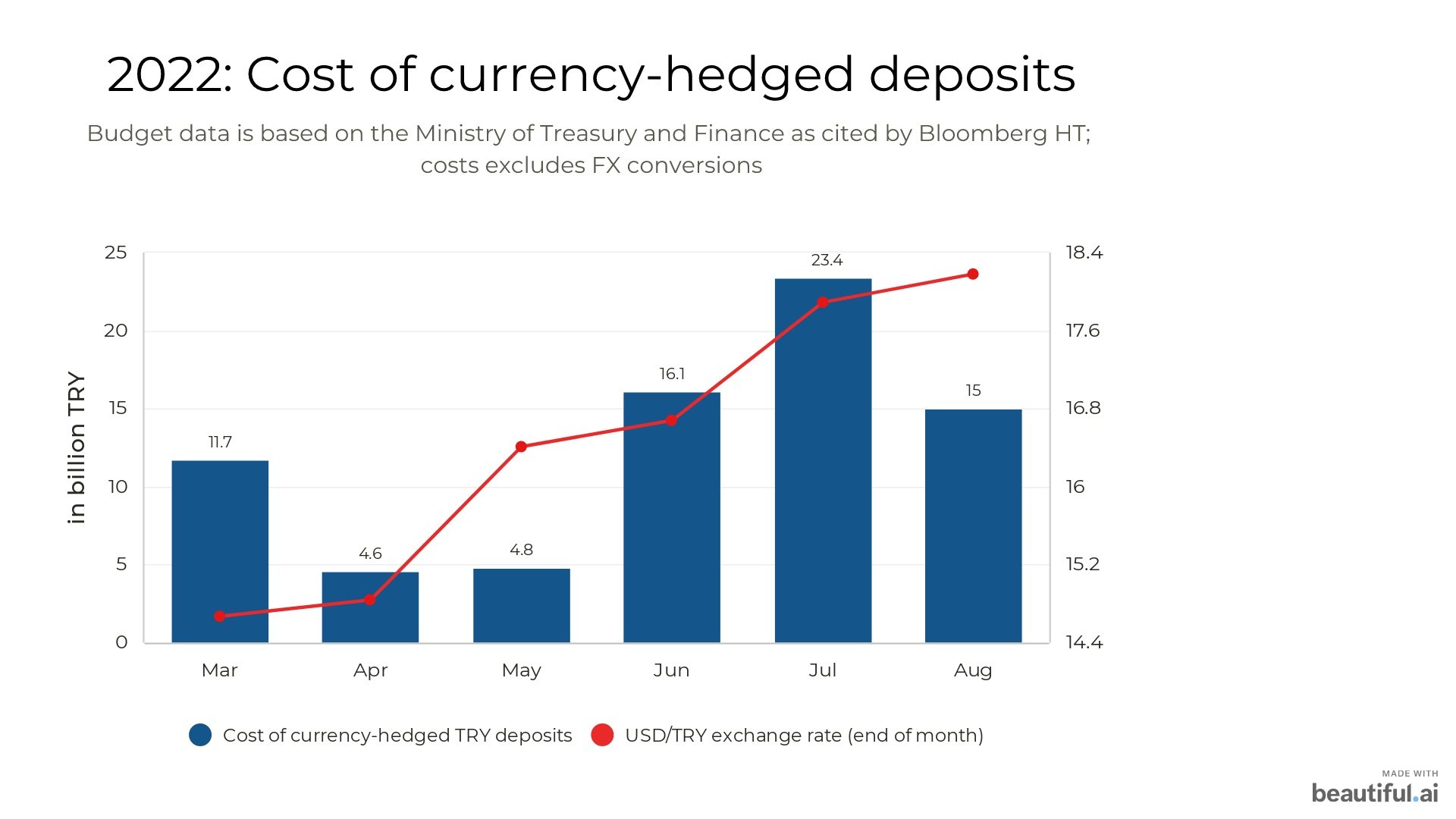

Bloomberg HT reports that the compensation for exchange rate losses to currency-hedged deposits from March to August was over 75 billion TRY (see graph below) and in the beginning of September the costs reached 1.3 trillion TRY.

The economy is functioning and growing at the cost of the currency and prices. Is this sustainable? So far it is working. For the future the answer is: we don’t know yet. We must wait and see.

* Disclaimer: The views expressed herein are those of the author and do not necessarily reflect those of the Deutsche Bundesbank or of the Eurosystem.