Turkish central bank: interest rate unchanged & a new swap deal

This article was first published on LinkedIn on January 21, 2022.

This week was a busy week at the Central Bank of the Republic of Turkey (CBRT). Here is a brief update and relevant topics to watch out for in the coming months.

What did Turkey's central bank announce yesterday?

Yesterday, the Turkish central bank announced the first interest rate decision of the year. As expected by market participants, the central bank decided to keep the policy rate unchanged at 14%. With this decision the central bank stopped the interest rate cuts, which started in September last year and intensified the downfall of the Turkish lira (loss of 44% in 2021).

Now, in the published press release the Turkish central bank emphasised that the review process of a comprehensive policy framework was carried out "with the aim of prioritising Turkish lira in all policy tools of the CBRT". This statement most likely hints towards a monetary policy targeting the foreign exchange in the coming time.

What about the inflation?

The past year has been tough for Turkish citizens with surge in prices for goods and services. Inflation rate hit 36% in December last year causing the central bank to halt the interest rate cuts. According to the press release "distorted pricing behaviour due to unhealthy price formations in the foreign exchange market, supply side factors such as the rise in global food and agricultural commodity prices, supply constraints, and demand developments" have led to an increase inflation. Lastly, the central bank expects the start of disinflation (i.e. fall in prices) process with the disappearance of base effects* in inflation and along with measures taken for sustainable price and financial stability.

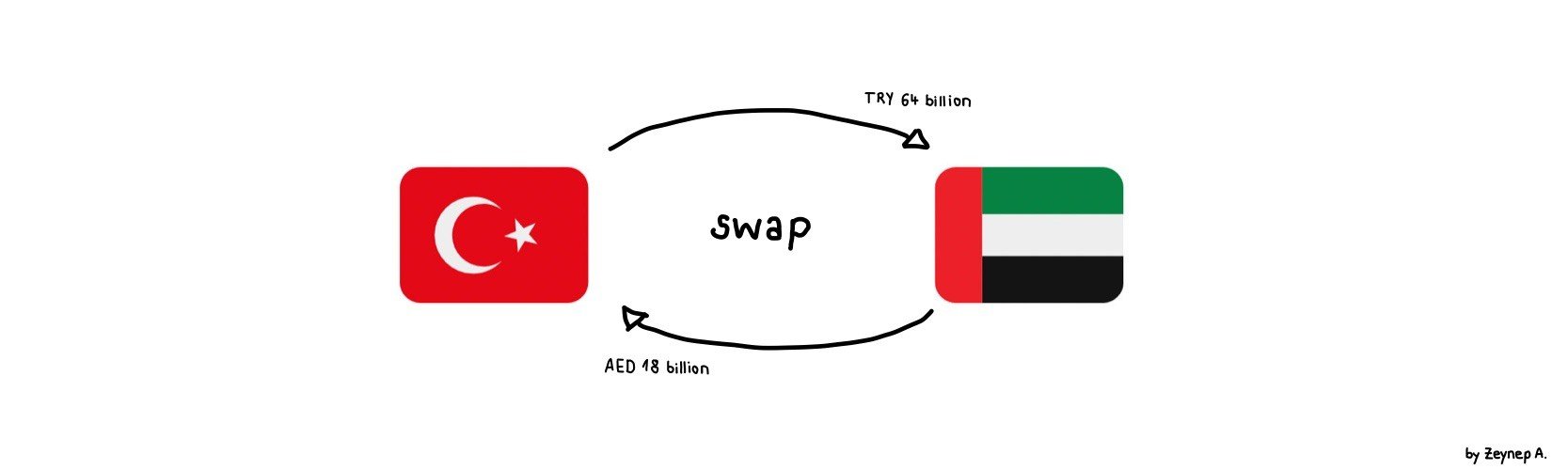

What about the swap deals made earlier this week?

On Wednesday, the Turkish central bank announced that it signed a swap agreement with the Central Bank of the United Arab Emirates (CBUAE). The bilateral currency swap agreement is in the local currencies of the respective countries, UAE Dirham (AED) and the Turkish lira (TRY). As stated on the website of the central bank the swap deal has a nominal size of AED 18 billion and TRY 64 billion (around USD 4.7 billion) and a three years period, with the possibility of extension.

Those so-called bilateral currency swap agreements between central banks emerged after the financial crisis in 2007 and allow domestic central bank to exchange currency with another central bank's foreign currency.** In Turkey's example this means that the Turkish central bank will receive UAE Dirham which it can then lend it to its domestic banks. Swaps between central banks are made mainly to boost reserves and lend foreign currency to its domestic banks and corporations. Additionally, bilateral swap agreements reflect trust between the two involved countries with the aim to promote cooperation on multiple levels, for example increased trade. In my next article I will look at currency swaps in more detail as this topic is a bit more challenging (and highly relevant for Turkish monetary policy).

* A good explanation of the base effect can be found here. Briefly, "[w]ithin the context of inflation, base effects refer to the impact of comparing current price levels in a given month against price levels in the same month a year ago."

** More details on central bank currency swaps can be found here by the Council on Foreign Relations (they have great illustrations!).

*** Disclaimer: The views expressed herein are those of the author and do not necessarily reflect those of the Deutsche Bundesbank or of the Eurosystem.